You don’t need a finance degree to understand how interest rates and central banks shape the economy. At first glance, terms like monetary policy, inflation targets, or rate hikes might seem complex — but once you break them down, it’s like learning a common language that explains why money behaves the way it does.

Let’s unpack this topic step by step — in a clear, friendly way.

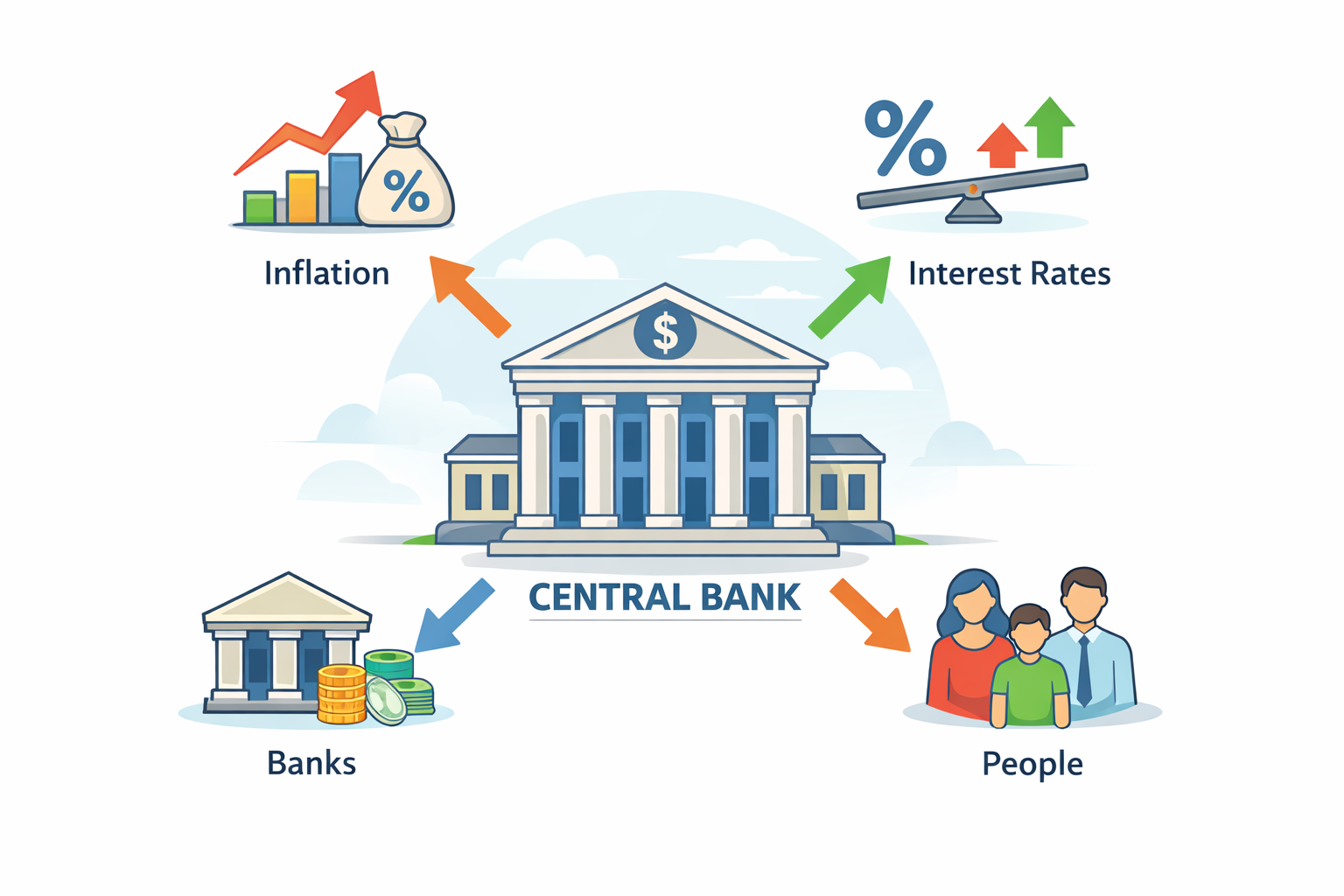

What Is a Central Bank?

Imagine the economy as a giant engine, and interest rates are one of the main levers that control its speed. The central bank is the mechanic — the one who adjusts settings to keep everything running smoothly.

In most countries, the central bank is the institution that:

- Manages the supply of money

- Sets benchmark interest rates

- Ensures financial stability

- Helps guide inflation toward a target

Examples include the Federal Reserve (U.S.), European Central Bank (ECB), Bank of England, and the Bank of Canada.

Their job isn’t to make profits (like commercial banks). Instead, it’s to maintain economic balance — a stable currency, low inflation, and steady growth.

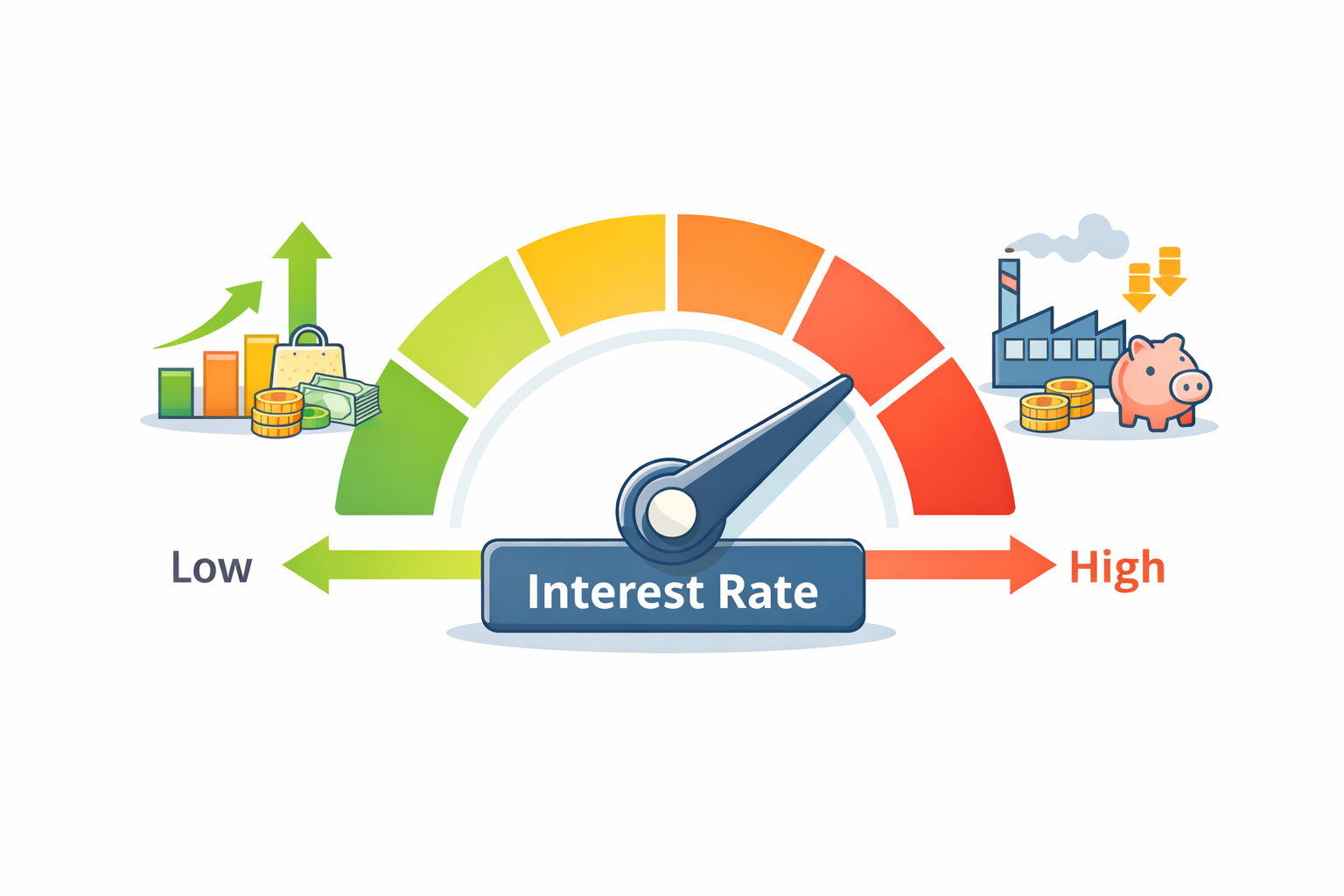

What Are Interest Rates?

In basic terms, an interest rate tells you how much extra you pay to use borrowed money, or how much you earn for letting your money sit with a bank (and the bank to use your money).

- When you borrow money, you pay interest.

- When you save money or let the bank use it, you earn interest.

For the economy, there’s a key interest rate called the policy rate (also called the base rate, repo rate, or federal funds rate, depending on the country). This is the primary tool central banks use to influence economic activity.

How Do Central Banks Use Interest Rates?

Central banks don’t just set one number and forget it. They constantly observe economic data — like inflation, unemployment, and GDP growth — and adjust interest rates to serve two broad goals:

1. Controlling Inflation

Inflation shows how much prices rise over time. A little inflation is healthy, but too much can erode purchasing power.

- High inflation → central bank may raise interest rates Higher rates make borrowing more expensive. People and businesses spend less, slowing demand and price increases.

- Low inflation (or deflation) → central bank may lower interest rates Lower rates make borrowing cheaper. That encourages spending and investment, boosting economic activity.

2. Supporting Economic Growth

Interest rates also help smooth the business cycle.

- In downturns, central banks often lower rates to encourage borrowing and spending.

- In overheated economies, they may raise rates to prevent excessive borrowing and asset bubbles.

Why Do Interest Rate Changes Matter to You?

Interest rate decisions can influence almost every part of your financial life:

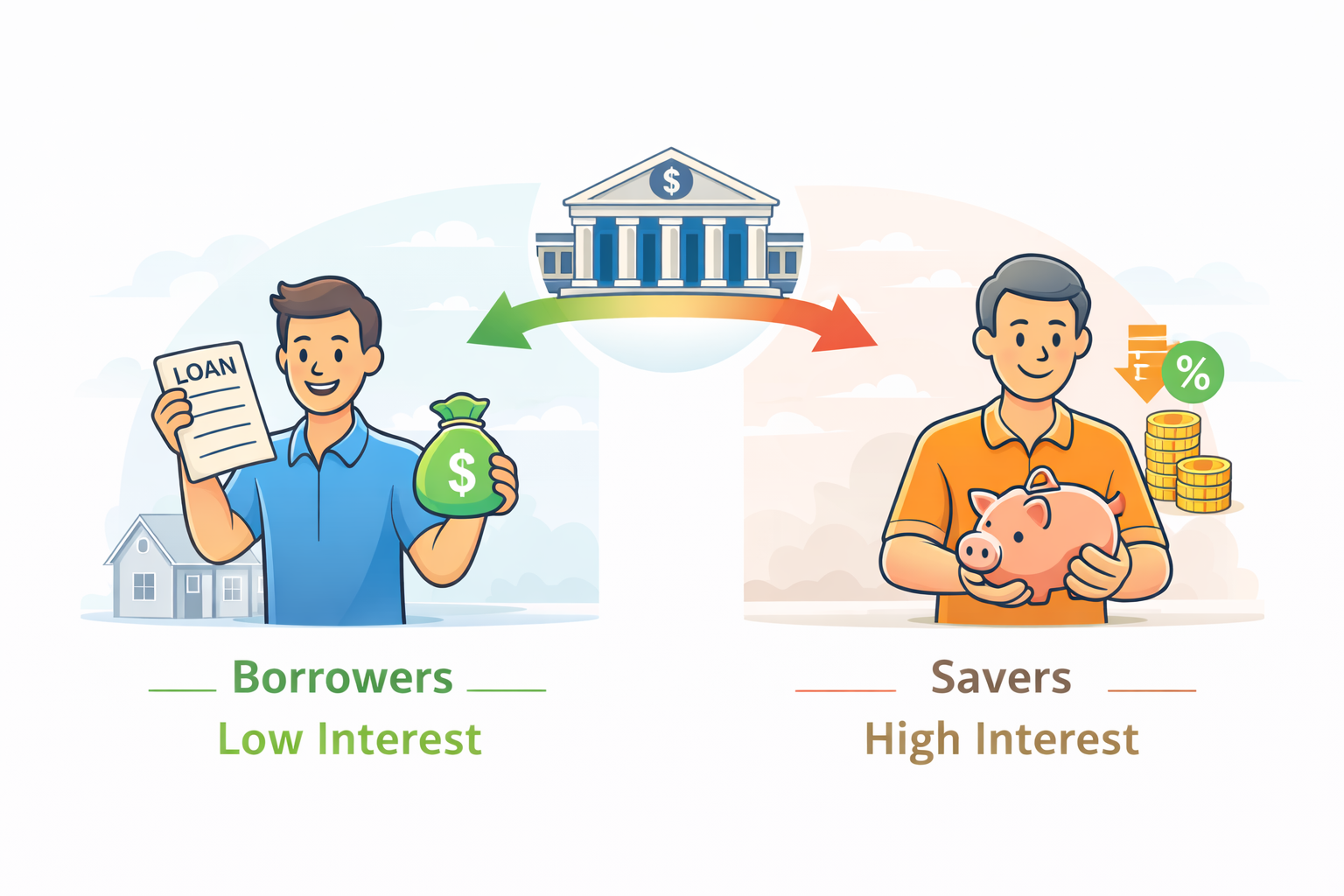

For Borrowers

- Lower rates → lower loan payments

- Higher rates → higher loan costs

So when central banks cut rates, mortgages, auto loans, and business loans often become cheaper.

For Savers

- Higher rates → better returns on savings accounts

- Lower rates → less income from savings

For Investors

Interest rate changes can affect:

- Stock market valuations

- Bond yields

- Currency exchange rates

Financial markets often react before the rate change happens, based on expectations. That’s why traders and investors pay close attention to central bank communications.

The Mechanism: How Do Rate Changes Work in Practice?

Here’s a simple example:

- The central bank lowers its policy rate (target interest rate).

- When policy rates are lowered, commercial banks can access central bank funds at a reduced cost.

- Commercial banks pass lower costs on to consumers — cheaper loans.

- Consumers and businesses borrow more.

- Increased spending stimulates economic growth.

Likewise, if the central bank raises rates:

- Borrowing costs increase.

- Consumers delay making big purchases (and don’t spend as much as before).

- Businesses reduce investment.

- Economic activity slows, which can cool inflation.

Central Bank Communication: Forward Guidance

Today’s central banks don’t just act — they talk. They use something called forward guidance — telling markets what they might do in the future. Why?

Because expectations matter.

If markets believe the central bank will raise rates next month, investors may adjust their portfolios now — even before any official change. This can flatten or steepen yield curves, shift currency values, and impact financial conditions.

A Simple Analogy

Think of the economy like a car:

- The central bank is the driver,

- Interest rates are the gas and brake pedals.

When the economy is slowing (like going downhill), the driver presses the gas (lowers interest rates) to keep up speed. When it’s speeding too fast (inflation rising), the driver taps the brake (raises interest rates) to regain control.

Recent Trends (Conceptually Speaking)

In the past decade:

- After major downturns — like the 2008 crisis or COVID-19 — central banks lowered rates to near zero to stimulate growth.

- As inflation picked up later, many central banks raised rates to cool price pressures.

This cycle — from easing to tightening — illustrates how monetary policy shifts depending on economic conditions.

Key Takeaways

Here’s what you should remember:

Final Thought

Interest rates and central banks may seem technical, but their impact is real and personal — from the price you pay on a loan, to the return on your savings, to the performance of investments. Learning how they work gives you an edge — whether you’re managing personal finances, investing, or simply curious about how economies function.